Most small business owners and single entrepreneurs start their business because they are good at what they do and want to take on the monetisation opportunities their offerings have. But running a business needs accounting and you cannot help but follow two major accounting methods, accrual vs cash basis accounting.

Choosing one of these two methods may put many entrepreneurs in a dilemma as they don’t have accounting expertise. But the method you choose for recording money in and money out can have a huge impact on how you see your business, how you plan for taxes, and how stable things are under the hood. This is why understanding these two accounting methods and their impact is so important.

This is not about impressing your CPA. It is about knowing what’s going on in your business when it counts, when you are deciding whether you can afford to hire someone, when tax time rolls around, or when you are pitching to a lender or investor.

So, this guide is here to explain the whole accrual vs cash basis accounting comparison with real-life examples and contexts.

Understanding What is What: Cash Basis vs. Accrual Basis Accounting

Let’s define these two methods along with use cases, one by one.

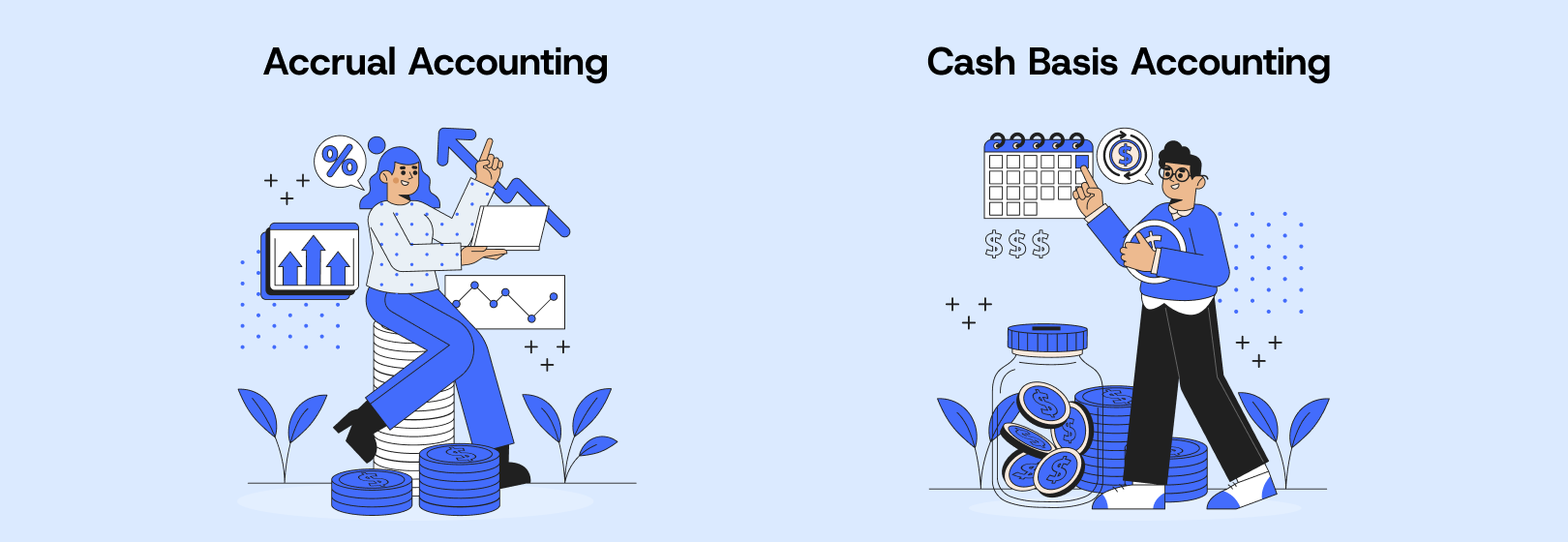

Cash Basis: You Count It When the Money Moves

This method is pretty straightforward. If you are using cash accounting, you only count money when it changes hands. That means income goes on the books when your customer pays you, and expenses show up when you pay the bill.

It is like the way most of us track our finances. If the money is in your account, it is real. If it is still “on the way,” you don’t count it yet.

Here is a quick real-world example:

For example, being a wedding photographer, you shoot a wedding on March 28, send the invoice right after, and the couple pays you on April 10. In the cash world, you don’t count that money until April 10, because that is when the cash hits your account. Until then, it is just a pending dream.

This is why the cash base method is also called small business accounting as it fits the accounting needs of small businesses, solo entrepreneurs, and freelancers. Any business that does not handle a lot of inventory and does not need to deal with complex and multilayered transactions, finds this method ideal for keeping their accounts organised and easy for evaluation.

Read More: Three Financial Statements:The Ultimate Guide

Accrual Accounting Explained: You Count It When You Earn It

Now, if cash basis is like tracking your wallet, accrual accounting method is more like tracking your promises. You recognise income when you earn it, and expenses when they happen, not when the money comes in or goes out.

Let’s now go back to our earlier example. You shot that wedding on March 28 and with accrual accounting, you would count that as March income, even if the check doesn’t land until April. That is when you did the work and delivered the value to your customer.

The same thing happens with expenses. If you get a bill for equipment rental in June but don’t pay it until July, the accrual method still considers that expense for June.

It is a little more complex, but it paints a truer picture of how your business is doing month to month. It is less about when money moves, and more about when the work and the corresponding costs are incurred.

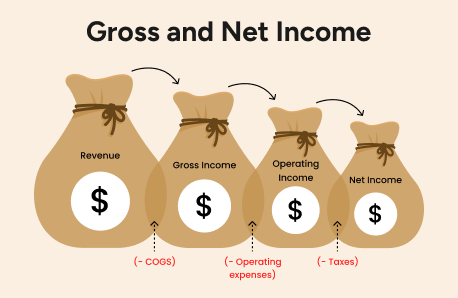

What’s the Real Difference in Terms of Impact?

The accrual vs cash basis accounting differences seem to be very little. But it is not.

Let’s explain through some real-life scenarios. In December, you onboard three big clients, invoice them all, and they pay you in January. If you are using the cash basis, your December income looks tiny and your January income looks like you hit the jackpot. But you did the work in December. So shouldn’t that be reflected in your numbers?

Accrual accounting method gives you a clearer view of your business performance because it lines up your revenue and your costs with the time they take place. It might be more work, but it gives you a much more honest view of how things are going.

Choosing the Right Accounting Method: What Fits Your Business

When it comes to small business accounting, they have a choice in how they track their finances. And the choice needs to make sense for how a business operates day to day.

When Cash Accounting Makes Sense: Keeping It Simple

If you are running a solo gig, maybe as a consultant, a web designer, or a dentist, you may not want to complicate accounting. You earn when cash hits your bank, and you spend when it leaves.

That is the cash accounting method in a nutshell. It is about seeing what’s actually in your account, not what someone promised to pay you next month.

Here is who can learn this way:

- Freelancers and contractors

- Solo service providers

- New side hustlers testing the waters

- Small operations with no inventory and fast payments

If you are not dealing with long-term contracts or large inventory purchases, a cash basis keeps your books clear and your stress levels low. You can look at your bank balance and know where you stand.

Accrual Basis: For When Things Get More Complex

Now, for example, a small but growing marketing agency signs a client with a $20,000 worth of business for the next four months. They pay you upfront. In a cash accounting world, it looks like you made $20k this month, but you know you’ll be working for that money over the next sixteen weeks.

That is the scenario where accrual accounting explained best. It helps you match income to when you earned it, not just when it landed in your bank. Same goes for expenses, if you order $5,000 in materials for a job you won’t deliver until next month, accrual lets you account for it when the work takes place.

Accrual works better for businesses that:

- Carry or sell physical inventory

- Deal with longer projects or contracts

- Offer subscriptions or monthly retainers

- Need to track receivables and payables accurately

- Are you looking for investors or applying for business loans

The accrual accounting method gives you a truer picture of your business’s actual performance. The kind of visibility that helps you plan, price, and grow without flying blind.

Same Business, Two Stories in Cash Flow

A small bakery that just received an upfront payment of $10,000 for a catering order. They received the upfront payment in March but the event is scheduled for mid-April.

- Under cash accounting, the statement will show $10,000 revenue in March.

- Under accrual accounting, it will record the income in April, when you deliver the service.

One method shows cash flow and the other shows operational timing. Both are valid, it just depends on what you are trying to understand.

IRS Rules: When It’s No Longer Optional

The IRS has rules. If your business crosses certain thresholds, either in revenue or in complexity, cash basis accounting stops being an option.

You are typically required to use accrual accounting if:

- Your gross receipts exceed $27 million and this amount adjusts for inflation each year.

- You are a C-grade corporation, or have a C-grade corporation as a partner.

- Your business carries inventory.

Accrual accounting is more about financial accuracy at scale. When your business gets bigger, simple books are not adequate anymore to accommodate the complexity, and hence accrual accounting becomes an inevitable choice.

Can You Switch Later?

Yes, but remember that switching is not just a settings change in QuickBooks. You’ll need to file Form 3115 with the IRS and you may need a professional to carry out this change.

Switching methods also means adjusting prior records through realigning the way past income and expenses were logged.

In any case, switching is highly doable, but it is always good to pick the right method from the very beginning.

How Your Accounting Method Impacts Cash Flow, Taxes, and Business Decisions (More Than You’d Think)

You know that feeling when everything looks fine in your bank account, until you realise you have a dosen unpaid invoices and a tax bill around the corner.

Let’s talk about why this choice is not just about bookkeeping, but very much about how you run your business.

Cash Flow: The Difference Between “Have It” and “Owe It”

When you are using the cash accounting method, you see money come in and the accounting book records it. When you pay out, it is gone from the books.

But this simplicity can be deceiving. You might land a few big deposits in a month and if that money is tied to work you have not delivered yet or business expenses you have not paid for, your account may still lack solvency.

Now with an accrual accounting method, you see future obligations and earnings in real time. You know you invoiced $8,000 last week, even if it has not hit your bank yet and you can plan your payroll accordingly.

Taxes: Timing Can Be Everything

Tax season is when a lot of small businesses get blindsided.

If you are on the cash basis, you are only taxed on money that came in. So if a client pays late, you have less taxable income this year. This flexibility can work in your favor.

But it comes as a double-edged sword. You could also get hit with a tax bill on income you already spent, because you did not track expenses or plan for timing differences.

On the other hand, accrual accounting smooths out these bumps. You record income when it is earned and expenses when they are incurred, so tax time reflects the real activity of your business, not just your bank activity. This way you can predict your taxes and be more transparently prepared.

Business Decisions: Why Seeing the Whole Picture Matters

When you are making hiring decisions, decisions on pricing changes, or taking investment calls based on just what is in your checking account, it can be simple if your business is small.

But as things get more layered, you need visibility and transparency ensured by accrual accounting, This method allows you to see what’s owed to you and your future obligations. You also get a better sense of gross margins and how your business performs over time.

Whether you want to pitch investors or apply for a business loan, you need to show accrual-based financials.

Can You Still Budget and Forecast on a Cash Basis?

You can, but it is harder and less accurate. Cash basis accounting doesn’t naturally give you insights into your receivables, liabilities, or future revenue. That means forecasting becomes guesswork.

Now, if you are super disciplined, and you have built manual systems to track everything in spreadsheets, you can still run a tight ship. But you are sailing against the tide.

Accrual gives you the tools upfront. You can spot trends, run profit-and-loss statements that reflect your operations, and get peace of mind knowing where things stand.

Final Thought

This is not about choosing the smart method or the professional method. It is about picking the system that helps you see your business.

If you are a solo founder just trying to survive the next quarter, a cash basis might give you the clarity you need. But if you are building toward a growth machine consisting of employees, vendors, investors, and strategic planning, accrual gives you that long-term visibility.

At the end of the day, your accounting method should help you make better decisions, not just check a box for the IRS.

![How Startups Can Leverage Financial Forecasting for Success [2025 Guide]](https://www.modelreef.io/wp-content/uploads/2025/04/Financial-Forecasting-for-Business-1.png)